When dealing with financial matters, having a "Power of Attorney (POA)" can be essential, especially when you need to manage someone else's finances. However, it can be frustrating when the bank refuses to honor a "Financial Power of Attorney" document. Understanding the reasons for this refusal and the steps you can take to resolve the situation is crucial. In this article, we will explore effective strategies to address this issue and ensure that the financial needs of the individual are met.

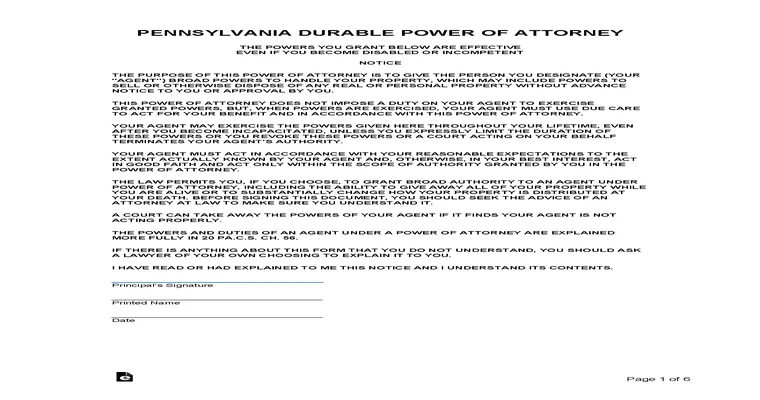

First, it is important to understand why the bank may refuse to accept a "Financial POA". Common reasons include the document not being properly notarized, the bank's internal policies, or the POA being outdated or lacking specific powers necessary for the transaction. Before taking any action, review the document to ensure that it complies with legal requirements and is up to date.

If the bank refuses to accept the "Financial Power of Attorney", the first step is to communicate directly with a bank representative. Request clarification on why the document was not accepted. This conversation can provide insight into any specific issues that can be easily addressed, such as providing additional documentation or updating the POA.

In some cases, it may be beneficial to present the "Financial POA" to a different branch of the same bank or even a different financial institution. Different branches may have varying policies or levels of familiarity with certain documents. If you encounter resistance at one location, do not hesitate to try another.

If the bank continues to refuse the "Financial POA", consider consulting with a legal professional who specializes in estate planning or elder law. An attorney can review the document, provide legal advice, and suggest modifications if necessary. They can also communicate with the bank on your behalf, which may lend additional credibility to your claim.

It may also be helpful to gather supporting documentation that reinforces the legitimacy of the "Financial Power of Attorney". This could include the principal's identification, proof of their incapacity (if applicable), and any other relevant financial documents. Having this information readily available can help to persuade the bank to accept the POA.

Another option is to file a complaint with the bank's customer service or ombudsman. Many financial institutions have procedures in place for handling disputes and complaints. By formally documenting your issue, you may prompt the bank to reevaluate their refusal and consider your request more seriously.

In extreme cases, if all else fails, pursuing legal action may be necessary. This approach can be lengthy and costly, so it should be considered a last resort. Legal action might involve petitioning the court to compel the bank to accept the "Financial Power of Attorney" or to seek damages for any financial losses incurred due to the bank's refusal.

In conclusion, when faced with a situation where the bank refuses a "Financial POA document", it is crucial to remain calm and methodical. Start by understanding the reasons behind the refusal, communicate effectively with bank representatives, and seek legal guidance if necessary. By taking these steps, you can work towards resolving the issue and ensuring that the financial affairs are managed as intended.