When it comes to financing long-term care or other significant expenses, many individuals often wonder about the benefits of a "promissory note". This financial instrument can be particularly relevant for those facing a "penalty period due to transfer". You might ask, why not just "private pay" from the start? In this article, we will explore the advantages of using a promissory note and clarify its role in navigating the complexities of payment for care services.

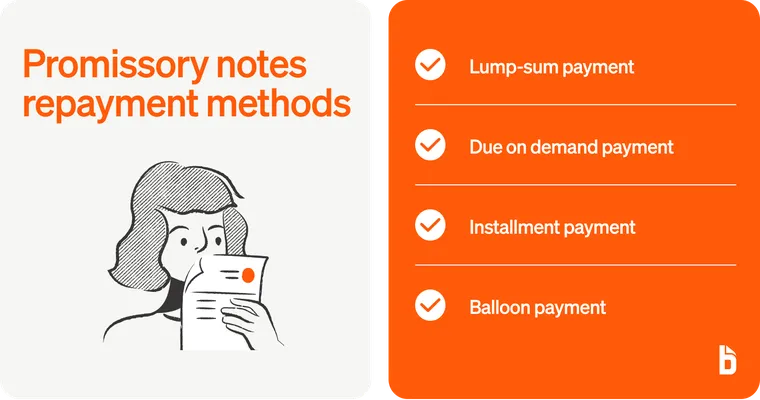

A promissory note is a legally binding document in which one party agrees to pay a specified sum to another party at a designated time. This financial tool can be especially beneficial when dealing with Medicaid and long-term care planning. One of the primary benefits of utilizing a promissory note is that it allows individuals to convert assets into a structured payment plan, which can help avoid penalties associated with transferring assets too quickly.

When you transfer assets to qualify for Medicaid, the state may impose a "penalty period" during which you will be ineligible for benefits. This penalty period is determined based on the value of the assets transferred. However, by using a promissory note, you can create a repayment schedule that outlines how much will be paid regularly over time. This structured approach can help mitigate the impact of the penalty period, as it demonstrates a legitimate need for funds to cover care expenses.

Moreover, a promissory note can be advantageous in preserving assets for your beneficiaries. Instead of outright gifting assets, which could trigger a penalty, you can use a promissory note to ensure that the funds are available to pay for care while still maintaining some form of asset transfer to your heirs. This strategic move can provide peace of mind, knowing that you are planning for both your care needs and your family's financial future.

Another reason to consider a promissory note over private pay is the flexibility it offers. With private pay, you may exhaust your savings quickly, especially if faced with high costs of care. In contrast, a promissory note allows you to manage your finances more effectively, enabling you to allocate funds over time while still qualifying for necessary benefits.

Additionally, promissory notes can be tailored to fit your specific financial situation. You can negotiate terms that suit both parties involved, whether it be the interest rate, payment frequency, or the total amount owed. This level of customization is often not available with standard private pay arrangements, which may have fixed terms and conditions.

In conclusion, while private pay might seem like a straightforward solution, the benefits of using a "promissory note" cannot be overlooked, especially in the context of navigating a "penalty period due to transfer". By opting for a promissory note, you can potentially save money, preserve assets for your heirs, and maintain a structured approach to financing your care needs. This makes it a valuable option for those planning for the future and seeking to manage their financial responsibilities effectively.